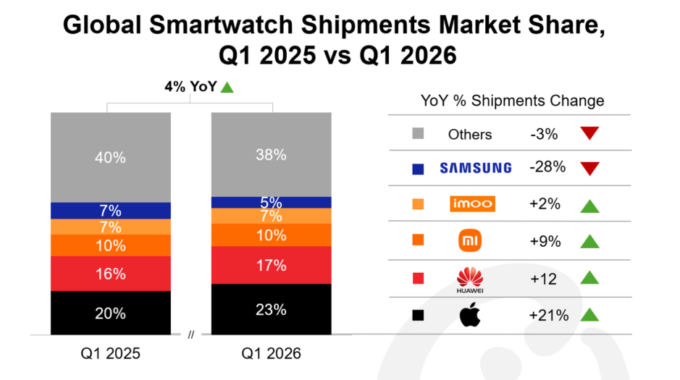

The global smartwatch market is holding steady. According to Counterpoint Research, global smartwatch shipments grew 4% year-over-year in Q1 2026, continuing the recovery that began in 2025 after a sluggish 2024. The two main forces behind that growth are Apple’s continued momentum across its refreshed product lineup and a strong rebound in China, where government subsidies and local brand enthusiasm have reignited consumer spending.

Apple took the top spot with 23% of global shipments, posting 21% year-over-year growth, the fastest of any brand in the top 10. In China, Huawei led the domestic market with roughly 40% share, followed by Imoo and Xiaomi. The wider China market grew 15% year-over-year, a number that reflects both policy support and a genuine shift in what consumers want from their wrists.

The numbers matter because smartwatches are no longer a novelty. Health tracking, AI features, and ecosystem integration are now buying decisions, not just selling points. That shift is pushing prices up and pulling new buyers in, especially in markets that were previously dominated by basic fitness bands.

Average selling prices rose 6% year-over-year in Q1 2026. Counterpoint’s Principal Analyst Anshika Jain points to two reasons: better sensors and AI capabilities built into mid-range and premium devices, and a broader upgrade cycle in emerging markets like India, where buyers are moving away from entry-level smartwatches toward more capable ones.

Apple’s growth was not limited to its home turf. While North America still accounts for more than half of Apple’s smartwatch shipments, China and Europe were its fastest-growing regions in the quarter. Two products drove that: the updated flagship Series lineup and the more affordable Apple Watch SE 3, which brought meaningful health features to price-conscious buyers.

Huawei’s story in China is worth watching closely. The company has been adding features that go beyond step counting, including:

- Sleep tracking

- Emotional wellbeing monitoring

- Arrhythmia analysis

Combined with a push across multiple price tiers and tight integration with Huawei’s broader device ecosystem, the brand has positioned itself as the default choice for health-conscious Chinese consumers. The extension of China’s government electronics subsidy scheme gave that momentum an additional boost.

The market’s recovery in 2025 came on the back of genuine product innovation. Brands introduced satellite connectivity, 5G RedCap support, AI-powered health insights, and clinically-relevant monitoring for conditions like sleep apnea and hypertension. Those features gave consumers real reasons to upgrade, which is why growth has held up even as the broader consumer electronics market has faced pressure.

That said, the road ahead has some bumps. Rising memory prices are a concern across the tech industry, and smartwatches are not immune. The good news is that smartwatches use relatively little memory compared to smartphones or laptops, so the impact on bill-of-materials costs should be smaller. Premium smartwatches also carry higher margins, which gives brands more room to absorb cost increases without passing them on entirely to buyers.

Counterpoint projects the smartwatch market will grow at a compound annual growth rate of 3% through 2030. That is not explosive, but it is consistent. For a category that was written off as a gimmick not long ago, steady growth driven by health, AI, and ecosystem lock-in tells a more durable story than the hype cycles that came before it.